Headwinds, Tailwinds and Crosswinds

- Overall housing starts fell 0.8% in March to a 1.42-million-unit annual rate.

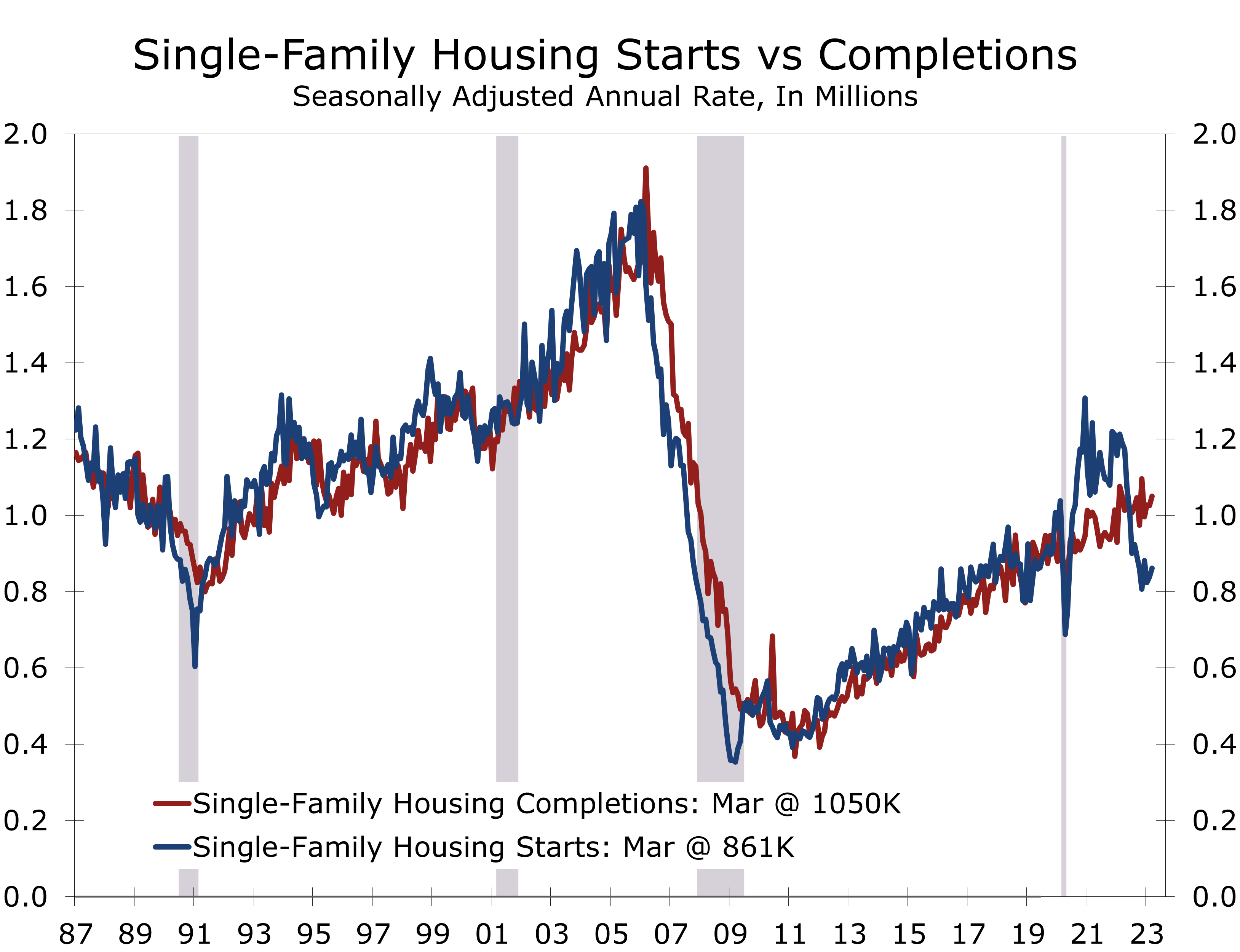

- Single-family starts rose 2.7% to an 861,000 unit pace, while multifamily starts fell 5.9% to a 559,000-unit pace.

- Permits moved more emphatically, with single-family permits rising 4.1% to an 818,000-unit pace, and multifamily permits tumbling 22.1% to a 595,000-unit pace.

- Milder weather boosted single-family starts earlier this year, so starts picked up less in March than usual, leading to a smaller seasonally adjusted gain.

- Permits are less impacted by the weather.

- The larger drop in multifamily permits might reflect some pause on the part of developers, amidst growing backlogs, slower rent growth and tightening credit.

- Single-family completions are now running well ahead of starts, helping clear backlogs.

- The backlog of apartment developments continues to increase and is now greater than any time since November 1973.

While overall housing starts fell slightly in March, there is a great deal of activity beyond the headlines. Overall starts fell 0.8% to a 1.42-million unit pace, with a modest 2.7%-rise in single-family starts partially offsetting a larger 5.9%-decline in multifamily starts.

Single-family starts are benefitting from lower mortgage rates, which have boosted new home sales. The National Association of Home Builders (NAHB)/Wells Fargo Home Market Index (HMI) rose 1 point in April to 45, marking its fourth consecutive increase. Home builders are feeling increasingly confident as mortgage rates appear to have hit a ceiling at around 7% last fall and have since fallen to around 6.5%. Rates are low enough to entice buyers into the market but are still well above the rate many homeowners have on their existing mortgages, which is keeping a lid on inventories of existing homes.

Builders are still discounting homes, but discounts are less prevalent and less generous.

Home builders are still discounting homes, primarily through mortgage rate buydowns, but discounts are less prevalent than a few months ago and less generous. The share of builders discounting prices fell to 30% in April, compared to 31% in March and February, and 35% in December and 36% in November.

The upturn in the HMI preceded a turnaround in housing starts. Unseasonably mild weather exaggerated the extent of the improvement earlier this year, which will tend to subtract from starts this spring.

Permits provide a clearer indication of where the housing market is today. Single-family permits rose 4.1% in March, following an 8.9% rise the prior month. The latest permit data likely reflect a turning point of sorts. Single-family permits most recently peaked in February of 2022 and declined steadily until January of this year, tumbling a cumulative 40%. So even after healthy back-to-back gains, single-family permits through the first three months of 2023 are running 31.2% below their year ago pace.

Home builders were bracing for a hard landing late last year when mortgage rates spiked.

Home builders were bracing for a hard landing late last year when mortgage rates spiked and briefly topped 7%. Inventories of unsold homes increased, as many would-be buyers were priced out of the market. Builders slowed new construction and ramped up incentives late last year, effectively buying down mortgage rates and discounting prices in some cases. Those incentives worked, and the correction in single-family construction has now largely been played out.

The correction in the multifamily market, however, is just getting started. Multifamily permits peaked for the cycle back in December 2021 at a 720,000-unit pace and declined through much of 2022. Permits rose again late last year, however, as developers raced to get projects started ahead of tightening credit conditions.

Apartment development is clearly overheated from an overall perspective. The pipeline of projects under construction has risen to 958,000 units – the most since November 1973. The backlog has set off alarm bells, as demand for apartments has shown signs of cooling and concerns about the health of the economy and banking system have increased.

The apartment market today is much different than it was back in 1973.

Much of apartment construction in the early 1970s was in low-rise garden apartments in suburban areas that were completed relatively quickly. Today, a much larger share of apartment construction is mid-rise and high-rise units that take considerably longer to build. As a result, we are less likely to face a sudden deluge of apartments. This is not to say that the apartment will not become overbuilt. Vacancy rates will almost certainly rise as the economy slows further and rents will likely decline modestly.

The correction in the single-family market is now well underway, with starts now running roughly 200,000 units below completions, which is helping reduce the backlog of homes under construction.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.