Business Owners Remain Weary

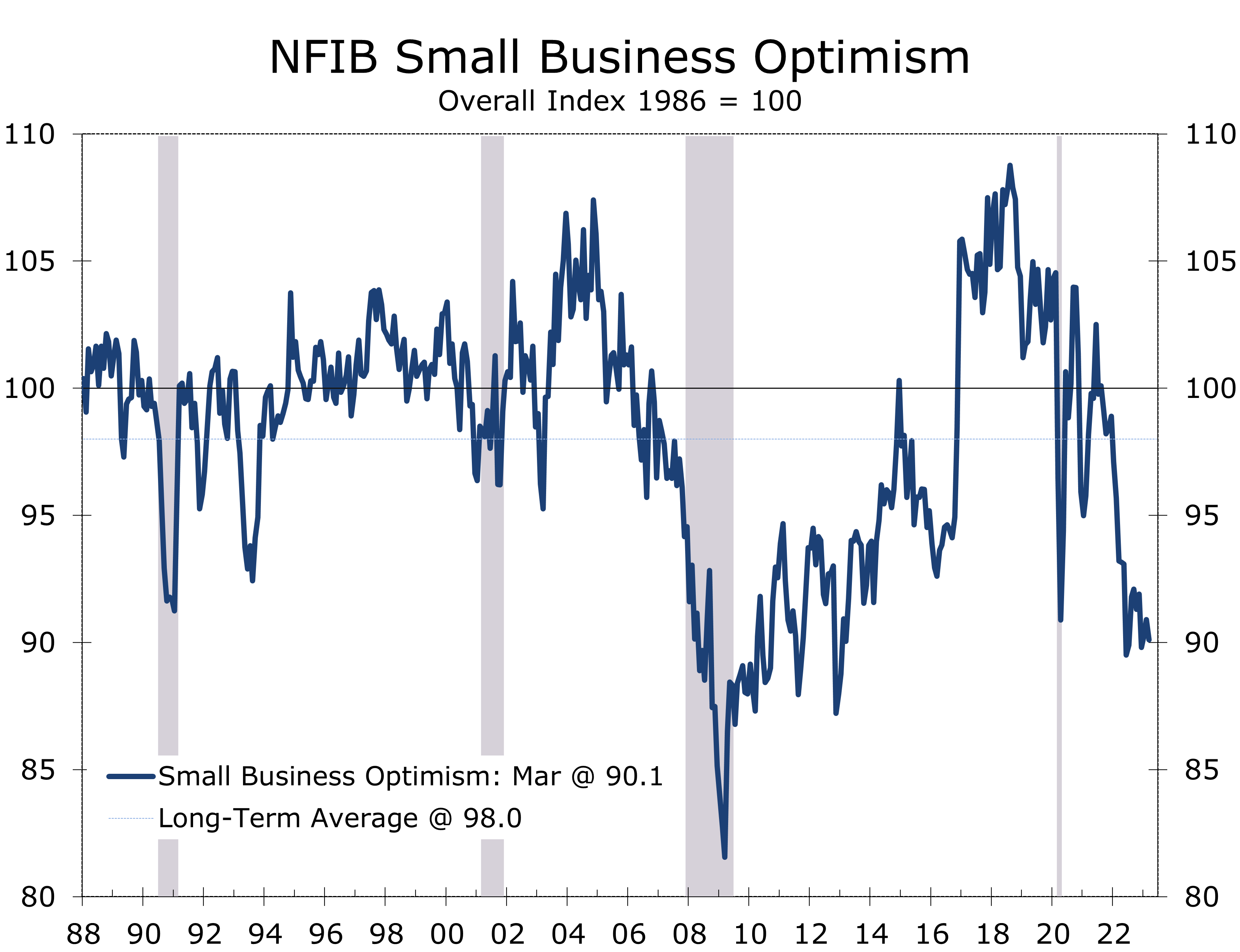

- The National Federation of Independent Business (NFIB) Small Business Optimism Survey fell 0.8 points to 90.1 in March, more than reversing the prior month’s rise.

- Small business owners remain deeply concerned about the overall economy, with the share of owners expecting the economy to improve over the next 6 months remaining unchanged at -47%.

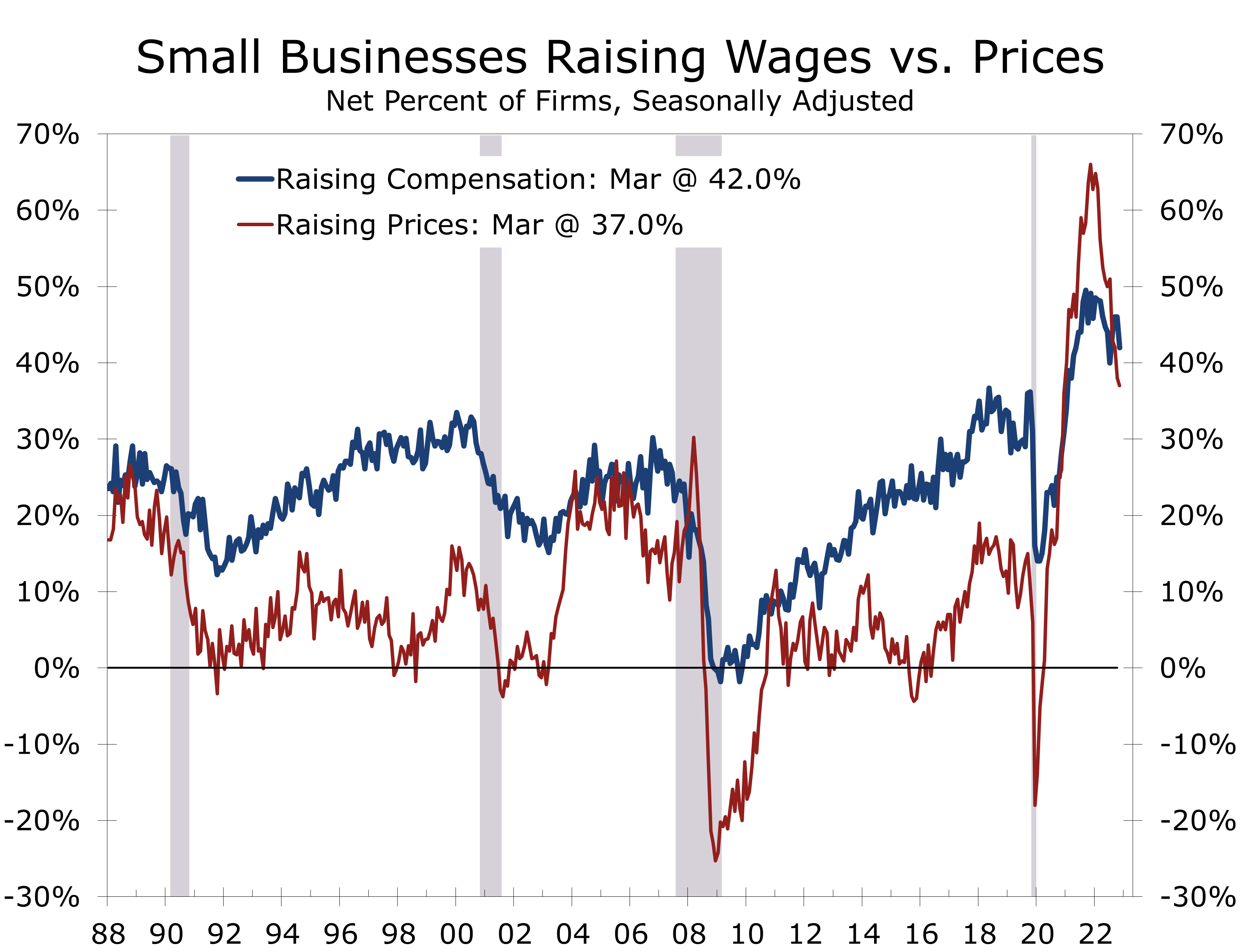

- Small business owners are continuing to get squeezed by weaking sales and stubborn wage costs. The share of firms expecting real sales to increase fell 6 points to -15%, while 42% of business report hiking compensation.

- The net share of businesses reporting they raised prices over the past 3 months fell 1 point to 37%, the lowest since April 2021.

- The share of businesses reporting their last loan was harder to secure than previous attempts rose 4 points to 9%.

Small Business Optimism fell 0.8 points in March to 90.1. The Optimism Index has remained below its long-term average for the past 15 months. Small business owners are increasingly frustrated that slower economic growth is negatively impacting their sales much more than it is helping alleviate long running hiring challenges or reducing labor and input costs.

Six of the Index’s 10 components fell in March, led by a 6-point drop in expected sales and a 4-point drop in both the share of business owners that feel now is a good time to expand and the share with current job openings. Expected credit conditions also deteriorated, falling 3 points to -9%. Plans to increase employment and plans to make capital expenditures fell 2 points and 1 point, respectively.

On the plus side, the share of small business owners that feel current inventories are too low rose 5 points to 1%. Coincidentally, the share expecting to increase inventories rose 3 points to a net -4%. The share of business owners stating they expect their earnings to improve also rose 5 points, although it remains deeply negative at -18%.

The NFIB index remains at levels more typically seen at the bottom of a recession.

Small business confidence has been extraordinarily weak for much of the past year and has been far weaker than the ISM survey or Consumer Confidence survey, both of which it has tracked historically closely. We suspect the discontent is due to the unusual swings in spending following the pandemic. The NFIB has closely tracked real GDP growth over this period, with real GDP rising a lackluster 0.9% over the past year.

One of the more closely watched areas of the NFIB survey this past month is the credit conditions. The March survey occurred late enough that business owners should have been aware of the collapse of Silicon Valley Bank and Signature Bank, as well as the likely implications for credit availability for their firm.

Credit conditions deteriorated in March, but they did not fall off a cliff.

The net share of business owners reporting it was harder to get a loan than it was previously rose 4 points in March to 9%. The 4-point rise marks the largest single-month gain since December 2002 and brought the series to its highest level since December 2012.

The tightening in credit is likely greater than what is shown in the latest NFIB survey. Only 26.9% of small business owners say they borrowed regularly during the past 12 months, while back in 2002 about 35% borrowed regularly. Businesses have also been reducing inventories this past year, which frees up cash and reduces borrowing needs.

That said, only 2% of owners reported that all their borrowing needs were not satisfied, down 1 point from February, and only 3% of business owners said that financing was their top business concern. The net share reporting paying a higher rate on their most recent loan rose 2 points to 26%.

The NFIB’s inflation measures have come down substantially this past year, although the improvement appears to be lessening and both measures remain high by historical standards. The NFIB survey is a diffusion index and provides insight into the breadth of price changes, as opposed to the magnitude of those changes. The breadth of price changes has been a reliable predictor of future inflation trends.

The net share of small businesses raising prices over the past three months fell 1 point to 37% in March and has fallen 29 points since peaking a year ago. The net share of firms planning to raise prices rose 1 point in March to 26%. Pricing plans also peaked a year ago and are down 26 points over that period.

Labor costs are proving stubborn, which will make it harder for firms to hold off hiking prices.

Pricing power has given way much faster than compensation costs have cooled off. The share of owners reporting compensation costs increased over the past three months fell 4 points to 42% in March but remains much closer to its highs than the share of firms raising prices. Both series remain historically high and suggest the Fed still has more work to do.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.