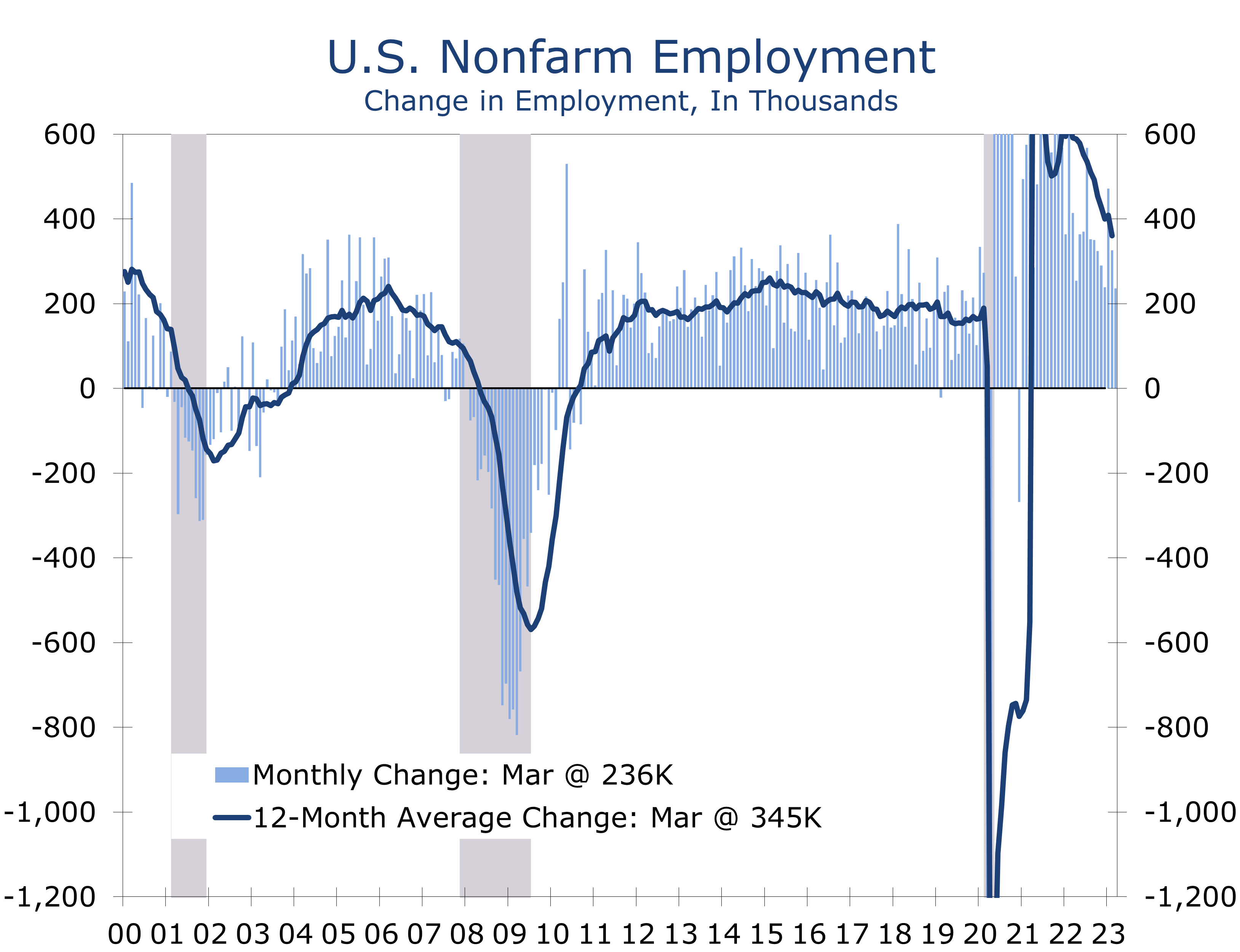

Q1 Will Likely Be the Strongest Quarter for Jobs

- Nonfarm employment rose by 236,000 in March. Revisions to the prior two months’ data subtracted a net 17,000 jobs.

- Private sector payrolls added a net 189,000 jobs in March, following gains of 266,000 in February and 353,000 in January.

- Job gains continue to be concentrated in industries that have generally struggled to add back workers. Leisure and hospitality added 72,000 jobs in March and health care and social assistance added 50,800 jobs.

- The most cyclically sensitive industries – construction (-9K) and manufacturing (-1k) lost jobs in March. In addition, temporary staffing firms cut 10,700 jobs.

- Aggregate hours worked edged 0.1 higher and rose at a 2.5% pace in Q1 – roughly equivalent with 3.5% real GDP growth.

- The civilian labor force participation rate rose 0.1 to a post-pandemic high 62.6.

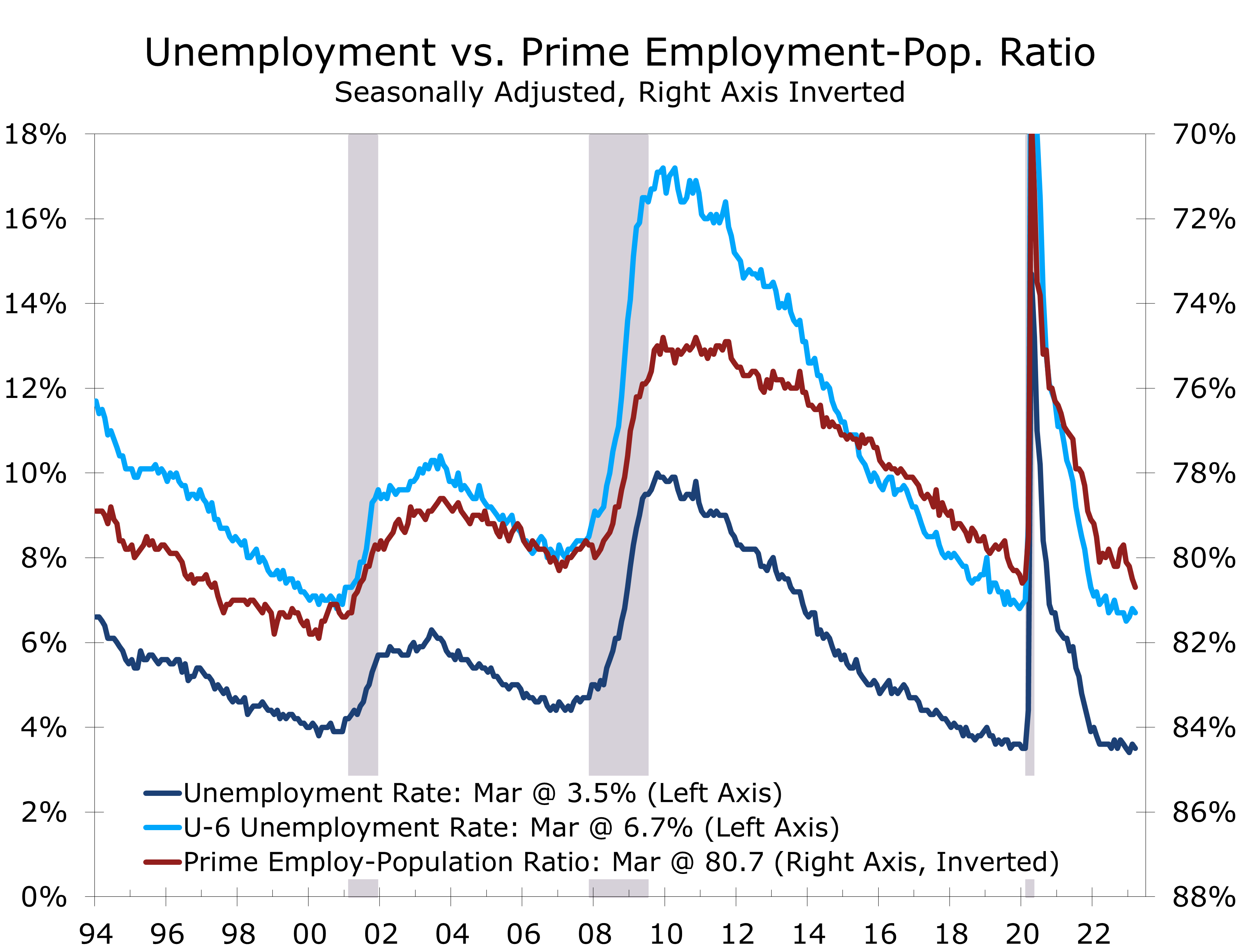

- The unemployment rate fell 0.1 point to 3.5%, while average hourly earnings rose 0.3% and are now up 4.2% year-to-year.

Employers added a net 236,000 jobs in March and average hourly earnings rose 0.3%. Data for the prior two months were revised slightly lower, subtracting 32,000 jobs from January’s previously reported gain but also adding 15,000 jobs to the February data.

The first quarter will likely be the high-water mark for job growth this year. Employers added a total of 1.034 million jobs during the quarter. A disproportionate share of those gains came from parts of the economy that have struggled to rehire, most notably the leisure and hospitality sector, certain parts of health care and social assistance, and government. These three areas accounted for two-thirds of overall job gains.

Even with recent outsized gains, restaurants and bars still largely remain understaffed. Payrolls in the leisure and hospitality sector remain 2.2% below their pre-pandemic levels, or 368,000 fewer jobs. Employment at nursing and residential care facilities also remains well below its pre-pandemic level, as do payrolls at private child care centers. Government payrolls are 1.4% below their pre-pandemic level, or 314,000 jobs.

Despite the recent outsized job gains, a few cracks are now emerging in the labor market.

We look for job growth to decelerate this spring, partly as a payback for an earlier than usual rise in payrolls due to unseasonably mild weather in much of the U.S.

More fundamentally, job growth is slowing in response to higher interest rates and the expectation that credit will tighten further in coming months. More and more businesses are focusing on cutting costs, which has led to a decline in job openings. The process is most apparent in the tech sector but has spread more recently to financial services and increasingly to most other industries.

Hiring in the most cyclically sensitive parts of the economy has clearly slowed. Construction employment, which was buoyed by unseasonably mild weather in January and February, lost 9,000 jobs in March. Manufacturing payrolls lost 1,000 jobs for the second month in a row, with notable losses in chemicals, fabricated metal products and semiconductor manufacturing.

Mining remains a bright spot, with oil exploration in the Permian Basin continuing to drive hiring. Midland and Odessa, Texas posted the fastest job growth over the past year of any metropolitan area, with hiring up 10.1% and 6.6%, respectively.

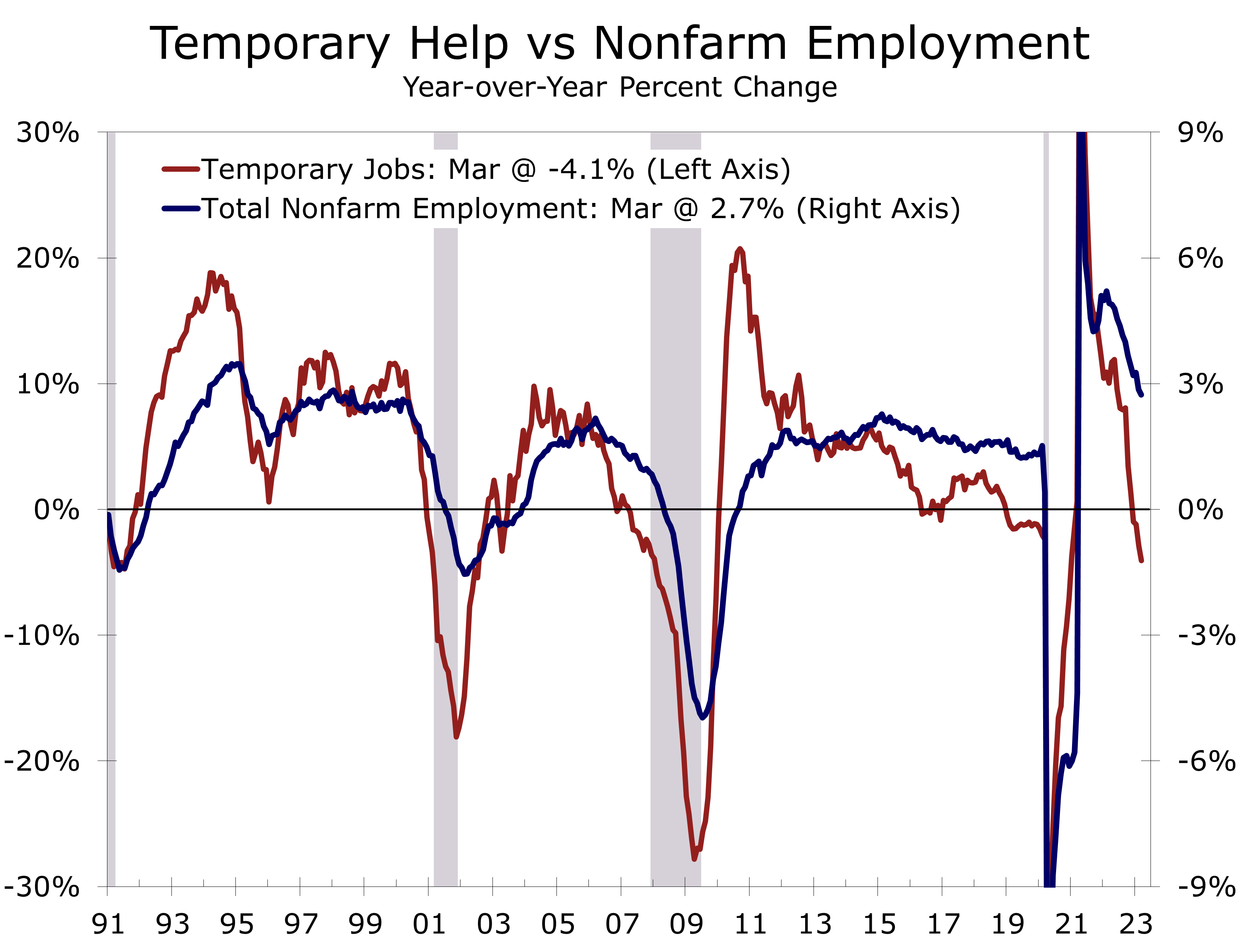

One of the more reliable leading indicators of payroll growth is the trend in hiring at temporary staffing firms, which has fallen 4.1% over the past year and is now at levels that have coincided with recessions in the past. Temporary staffing firms cut a net 10,700 jobs in March and have lost 146,500 jobs over the past year.

While the swoon in temporary staffing jobs looks ominous, most economic indicators continue to point toward a soft landing, at least in the near term. Job gains are still broad based, with 60.2% of industries adding jobs in March. Hiring is less broadly based than it used to be, however, with March marking the third smallest share since the start of the pandemic.

The unemployment rate fell 0.1 point to 3.5%.

The unemployment rate fell 0.1 point to 3.5% in March, as household employment rose by 577,000, outpacing a 480,000 rise in the civilian labor force. The labor force participation rate and prime employment population rate both rose in March, rising to their highest levels since the pandemic. The prime employment-population ratio rose 0.2 points to 80.7 and is now slightly higher than before the pandemic.

Given the latest employment data, the Fed is inclined to continue leaning toward another quarter-point interest rate hike at the May FOMC meeting. The May meeting will precede the April employment data, so March inflation reports are now front and center. The key report for the Fed, however, will likely be the April ISM report that will be reported on May 1.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.