Lower Rates Bring Buyers Back

- The National Association of Realtors reported that existing home sales surge 14.5% in February, which marks the largest increase since July 2020.

- The surge in existing sales reflects closings on contracts written in December and January when mortgage rates briefly fell back toward 6%.

- February is normally a slow month for home sales, so the seasonal adjustment is one of the largest of the year, which exaggerated the extent of the resurgence in sales.

- Sales were bolstered by the return of buyers that were priced out of the market when mortgage rates surged last fall and milder than usual weather across much of the US.

- Even with the surge in sales, homes are remaining on the market longer and prices are falling.

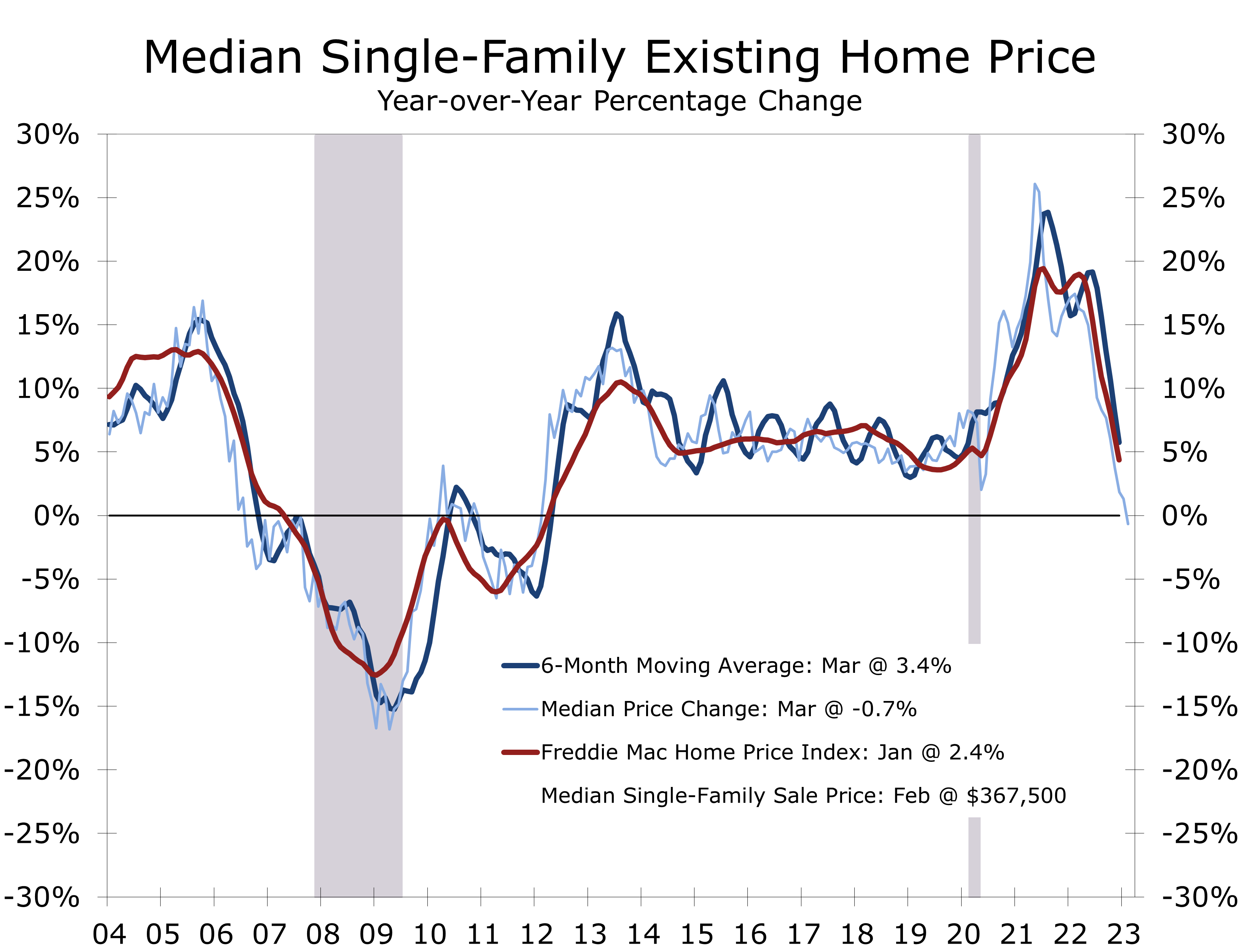

- The median price of an existing home has now fallen 0.2% over the past year, the first year-to-year decline since February 2012.

Sales of existing homes easily blew past expectations in February, with overall sales surging 14.5% to a 4.58 million unit rate. Sales of single-family homes rose an even larger 15.3% to a 4.14-million-unit pace, while sales of condominiums and co-ops rose 7.3% to a 440,000-unit pace.

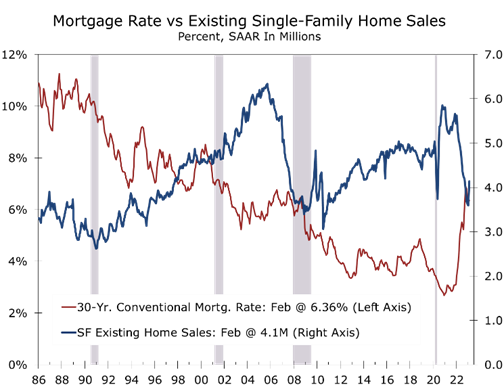

February’s jump in sales, which was three times the consensus estimate, was fueled by a sharp pull back in mortgage rates in late December and January, when mortgage rates briefly fell back to 6%. Mortgage lenders likely dialed up clients that saw sales fall through as many buyers that had written contracts early last fall found they no longer quailed when mortgage rates surged to 7%. Milder weather also helped, as February is usually one of the slowest months for home buying.

The wide swings in home sales and mortgage rates mean last fall’s weakness was overstated.

The wide swings in home sales and mortgage rates mean last fall’s weakness was likely overstated, just as February’s resurgence now is. Some analysts have even gone as far to say that home sales bottomed last fall and look for sales to steadily increase this year. We doubt it, as mortgage rates have already rebounded, and housing affordability remains historically challenging. After averaging 6.36% in February, mortgage rates rose steadily during the first half of March and are currently around 6.75%.

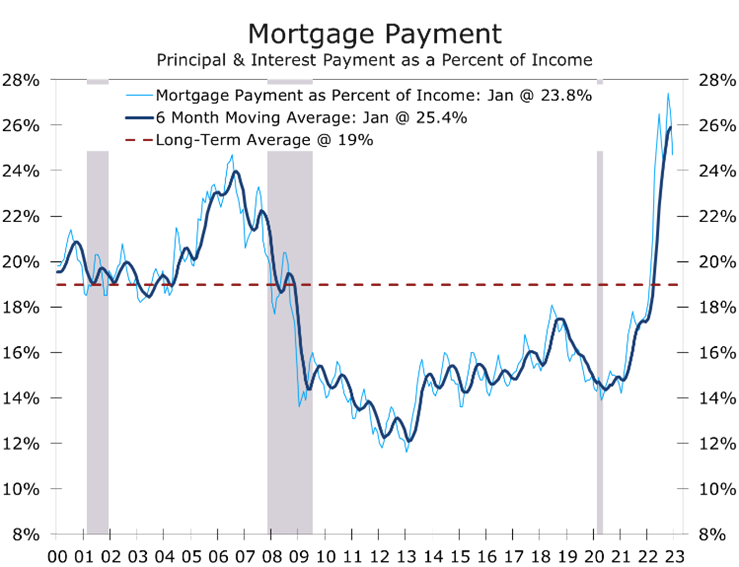

Lower mortgage rates and falling home prices had begun to make some inroads at restoring housing affordability. Qualifying income for a family earning the median income and purchasing the median price home has fallen 11% since October, from $98,064 to $86,736. The drop reflects the pullback in mortgage rates from 6.98% in October to 6.35% in January. The median price of an existing single-family home fell 5.6% over that 4-month period and is now down 13.7% since peaking in June.

Unfortunately, homeownership is still out of reach for far too many households. Monthly principal and interest payments for that median home totaled $1,807 in January, down from $2043 in October. Monthly principal and interest payments still consume an outsized 23.8% of median family income, which is roughly equivalent to what it was at the peak of the housing bubble 15 years ago.

For affordability to return to its long-run average, mortgage rates would need to fall more than a percentage point lower and home prices would have to fall further, while median family income increased. All those things are likely to eventually happen, but they will not happen quickly. Moreover, we are likely to see family income growth slow as job growth weakens. Credit underwriting will also likely tighten.

Home prices edged higher in February, with overall prices climbing 0.5% to $363,000 on a non-seasonally adjusted basis and prices of single-family homes rising 0.6% to $367,500. The gains mark the first increases in 8 months. Overall prices are down 12.3% since June of last year, while single-family prices have fallen 12.7%.

The median price of an existing home has fallen 12.3% since June and is down 0.2% year-to-year.

Home prices are now down 0.2% on a year-to-year basis and such comparisons are likely to deepen over the next 4 months, as comparisons with peak home prices will become more difficult.

February’s surge in existing home sales likely makes the Fed’s decision a little easier. We expect the Fed to hike the federal funds rate by a quarter percentage point at the conclusion of the FOMC meeting tomorrow and expect the target for the terminal funds rate for the cycle to come down from 6% to around 5.5%. The crisis surrounding Silicon Valley Bank and other West Coast Specialty lenders will likely result in some tightening of credit conditions ahead of the release of bank stress-test results in June. This will effectively do some of the Fed’s work for them.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.