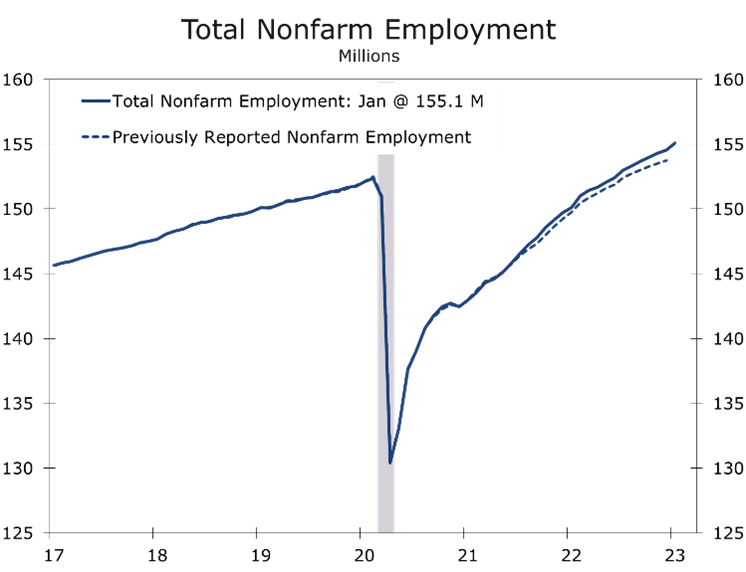

Employment Surges in January

- Nonfarm employment surged by 517,000 jobs in January, which was more than double consensus estimates.

- While hiring was led by another big jump in hiring at restaurants and bars, job gains were extremely broad based.

- The most cyclical parts of the economy -construction, manufacturing and trucking and warehousing – added a combined 66,900 jobs.

- Seasonal factors bolstered the overall job growth. More cautious holiday season hiring at retailers and delivery firms resulting in fewer than usual layoffs and a big seasonally adjusted gain in January.

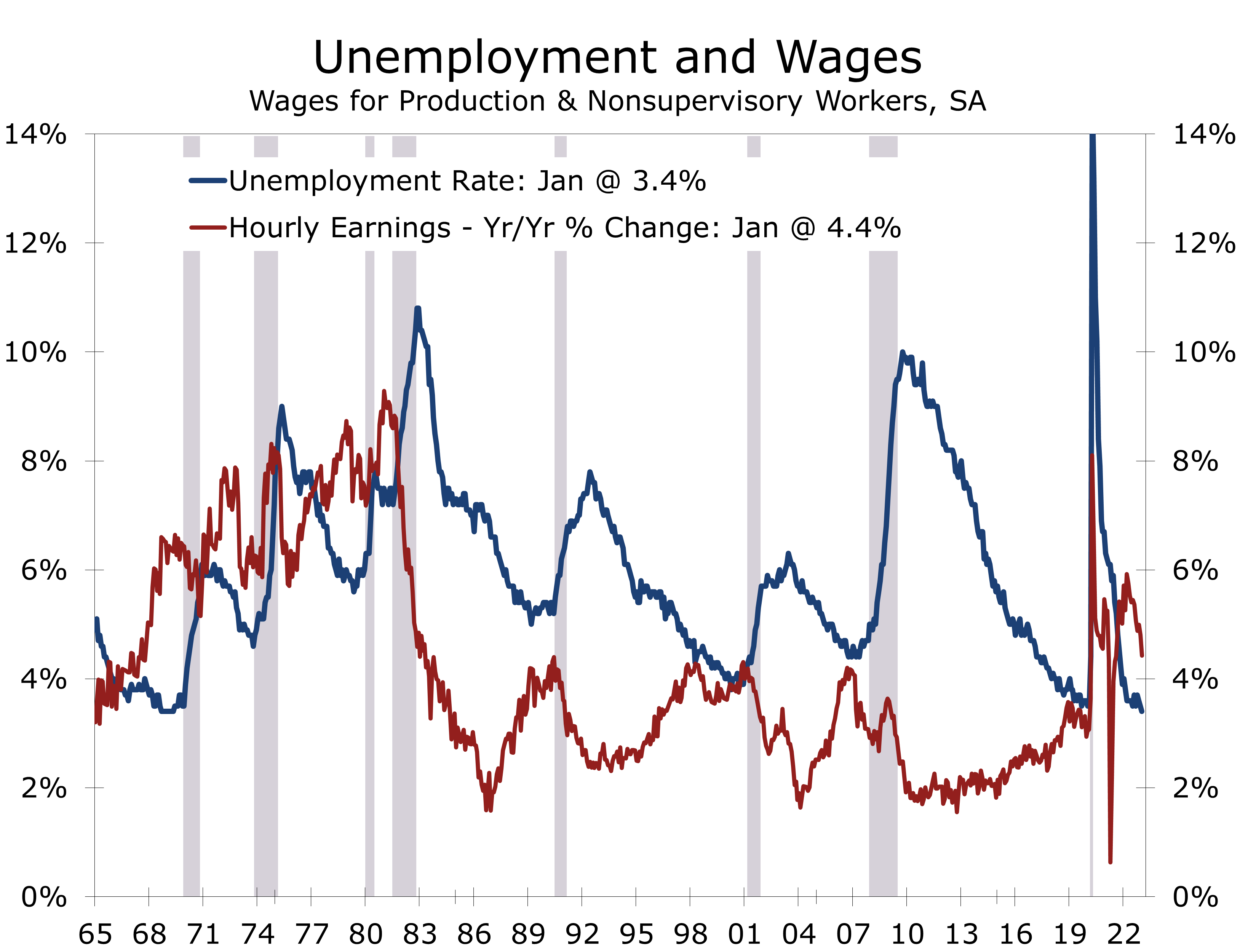

- The unemployment fell 0.1 percentage point to 3.4%, while average hourly earning rose 0.3% and are now up 4.4% year-to-year.

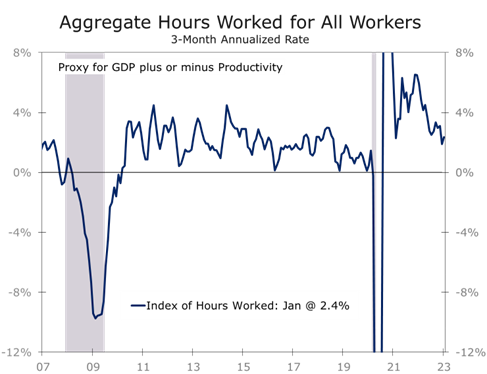

- Aggregate hours worked rose a whopping 1.5% in January, which pushes any thoughts about a recession at least a few months out.

There is quite a bit to unpack from this morning’s surprisingly strong employment report. The bottom line is job growth remains exceptionally strong. The January data include annual revisions to nonfarm employment, which incorporate more precise data on hiring. The benchmark revisions, combined with more complete reporting for the prior two months, show there were 813,000 more jobs on nonfarm payrolls in December than first reported. The benchmark revision was three times as large as normal.

Population estimates in the Household Survey were also adjusted to updated population estimates from the Census Bureau. The new data show a 1.1 million increase in the civilian population, and large related increases in the civilian labor force and the household employment measure. There was no net effect on the unemployment rate, which fell to 3.4%. The adjustment boosted the civilian labor force and employment-population ratio by 0.1% each. Both would have been unchanged without the new controls and will likely be reversed in February.

We believe it is still too early to assess the impact of the recent surge in tech layoffs.

The stronger nonfarm employment data appear to contradict the rising number of layoff announcements, most of which are in the tech sector. Weekly first-time unemployment claims have continued to trend lower. We believe it is still too early to assess the impact of layoffs. While employment fell slightly in some tech categories, many displaced workers will not fall off employer payrolls until March. This means these losses will show up in the March and April employment reports, which will be released in April and May.

The upward revision to nonfarm employment also appears to contradict the findings of a recent Federal Reserve Bank of Philadelphia report, which pointed out job growth for the second quarter of last year appeared to be overstated by around 1 million jobs. That survey highlighted to the gap between the Quarterly Census of Employment and Wages (QCEW), which are the source data for the annual benchmark revisions, and the reported CES data. The Benchmark revision, the bulk of which stretches back to March 2021, would not include the second quarter 2022 QCEW data. So, today’s large upward revisions do not refute the Fed study.

The 2022 nonfarm data will be revised once again next February, and we will get some idea of the scope of those revisions when the QCEW data for the third quarter of 2022 will be released on February 22. Our sense is we will a see sizable downward revision next February. There are a whole host of government and private sector data that show economic activity moderating considerably since March 2022, which is when the Fed began to hike interest rates.

Even if we do see a downward revision to the 2022 employment data next year, the labor market clearly looks much stronger today. Any notion of an imminent recession has been pushed further out. Hiring rose across nearly every major industry in January, with even the most cyclical industry segments – construction, manufacturing and transportation and warehousing – adding a combined 66,900 jobs.

The factory workweek rose by 0.4 hours to 40.5 hours, and overtime hours rose 0.1 hour to 3.1 hours. The rise in hours suggests manufacturers are still looking to add workers. This is somewhat surprising given January’s weaker ISM-Manufacturing report and a whole host of weaker regional manufacturing surveys but is consistent with the rise in job openings. Total hours worked in manufacturing – a reliable predictor of industrial production – rose 0.9% in January.

One reason economists closely scrutinize the monthly jobs data is they provide clues about data for the rest of the month. In addition to a rise in industrial production, consumer spending should also rebound, following back-to-back declines. We come to that conclusion by combining the 1.2-point surge in aggregate hours worked and 0.3% rise in average hourly earnings.

The smaller rise in average hourly earnings likely reflects more hiring in lower paid occupations and some moderation in hiring for higher paid jobs. With the unemployment rate now at its lowest level since May 1969, we can expect the Fed to continue raising interest rates for at least the next couple of meetings.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.