A Busy Day for Economic News

- The Fed raised its federal funds rate target a quarter percentage point to between 4.50% and 4.75%. The Fed also indicated ongoing increases will be appropriate.

- Consumer spending rose at a solid 2% pace, with the strongest gains coming in services.

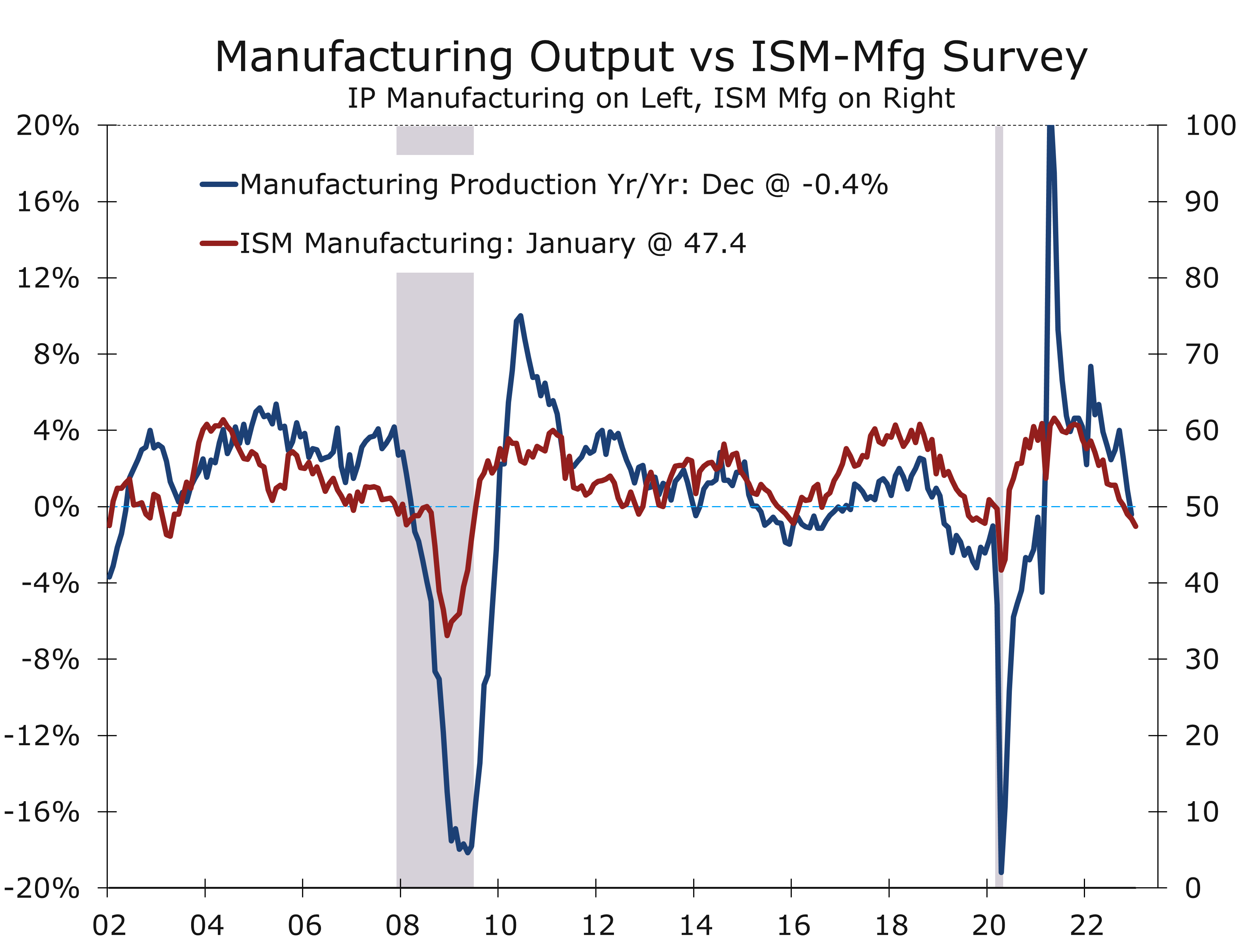

- The ISM Manufacturing Index fell 1 point to 47.4 in January, marking the fifth consecutive monthly drop.

- Overall construction spending fell 0.4% in December. Spending for private single- family homes fell a particularly sharp 2.3%.

- The ADP employment report showed hiring slowed in January, with private sector businesses adding 106,000 jobs, following a 253,000-job gain in December.

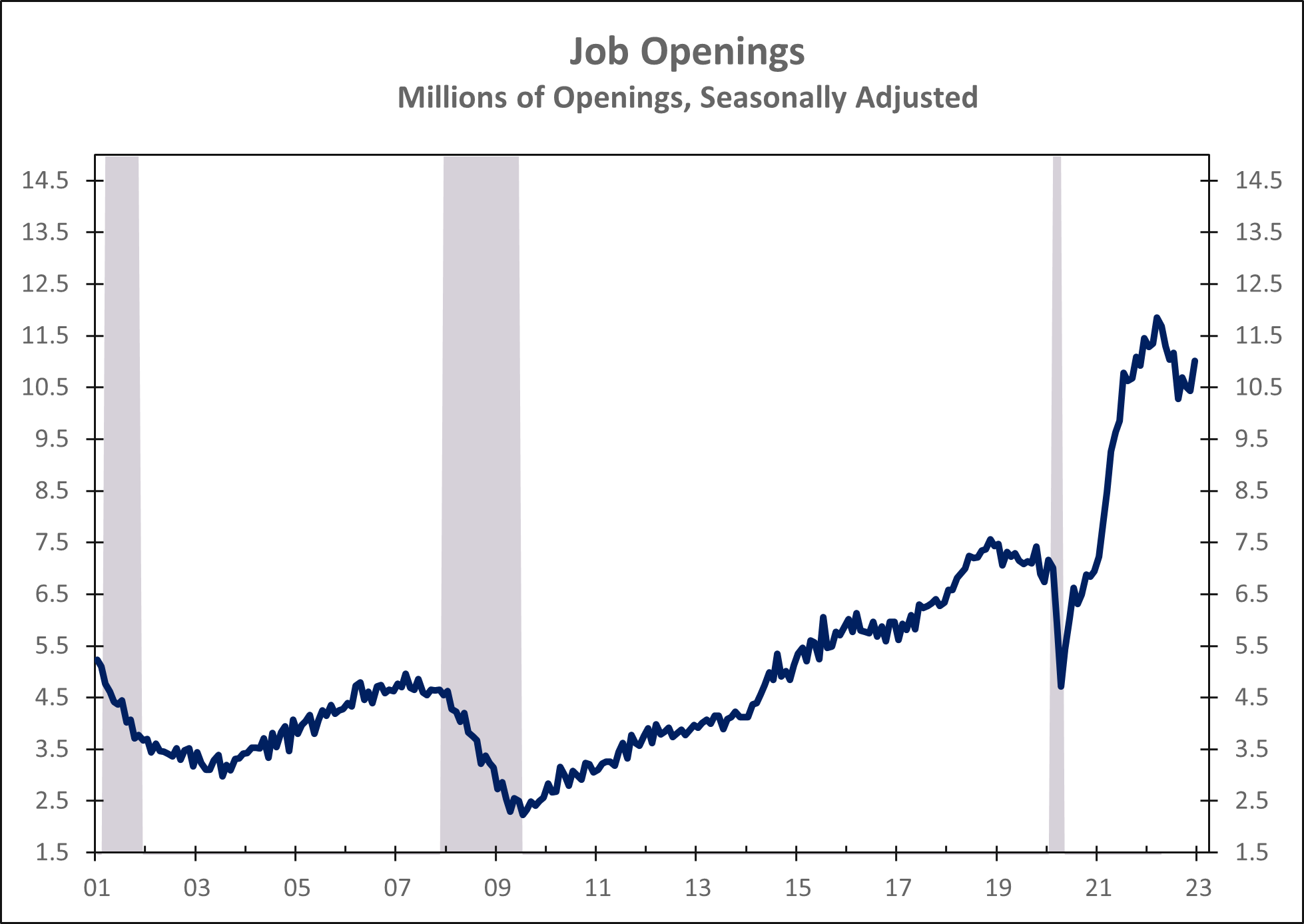

- Job Openings increased by a larger than expected 572,000 in December to 11 million. The bulk of the increase was in the leisure and hospitality sector. Openings fell in the IT sector and in manufacturing.

The Federal Reserve raised interest rates precisely in line with market expectations. The range for the federal funds rate target was increased by a quarter point to between 4.50% to 4.75%. The FOMC also noted they anticipate “ongoing increases in the target range will be appropriate.” Our read is the Fed is looking past the easing in supply chain inflation pressures and now sees tight labor markets and rising wages as the greatest risk to inflation.

The Fed’s assessment of economic conditions in the meeting’s Policy Statement was surprisingly upbeat, noting “recent indicators point to modest growth in spending and production.” The most recent data, however, show back-to-back declines in real consumer spending and three consecutive declines in industrial production. This morning’s ISM manufacturing survey shows even more convincing weakness, with the index declining for five consecutive months and hinting industrial production fell once again in January.

Employment conditions remain too strong for the Fed to end their policy tightening.

Employment conditions appear to be closer to the Fed’s assessment, which noted “job gains have been robust in recent months, and the unemployment rate has remained low.” The latest data are clearly supportive of that view, with weekly first-time jobless claims, the unemployment rate at 50-year lows and job openings rising by a surprisingly 572,000 to just over 11 million in December. Even this morning’s weaker ISM survey showed employment conditions in the factory sector remaining in positive territory, possibly suggesting manufacturers are hoarding working amidst and exceptionally tight labor market.

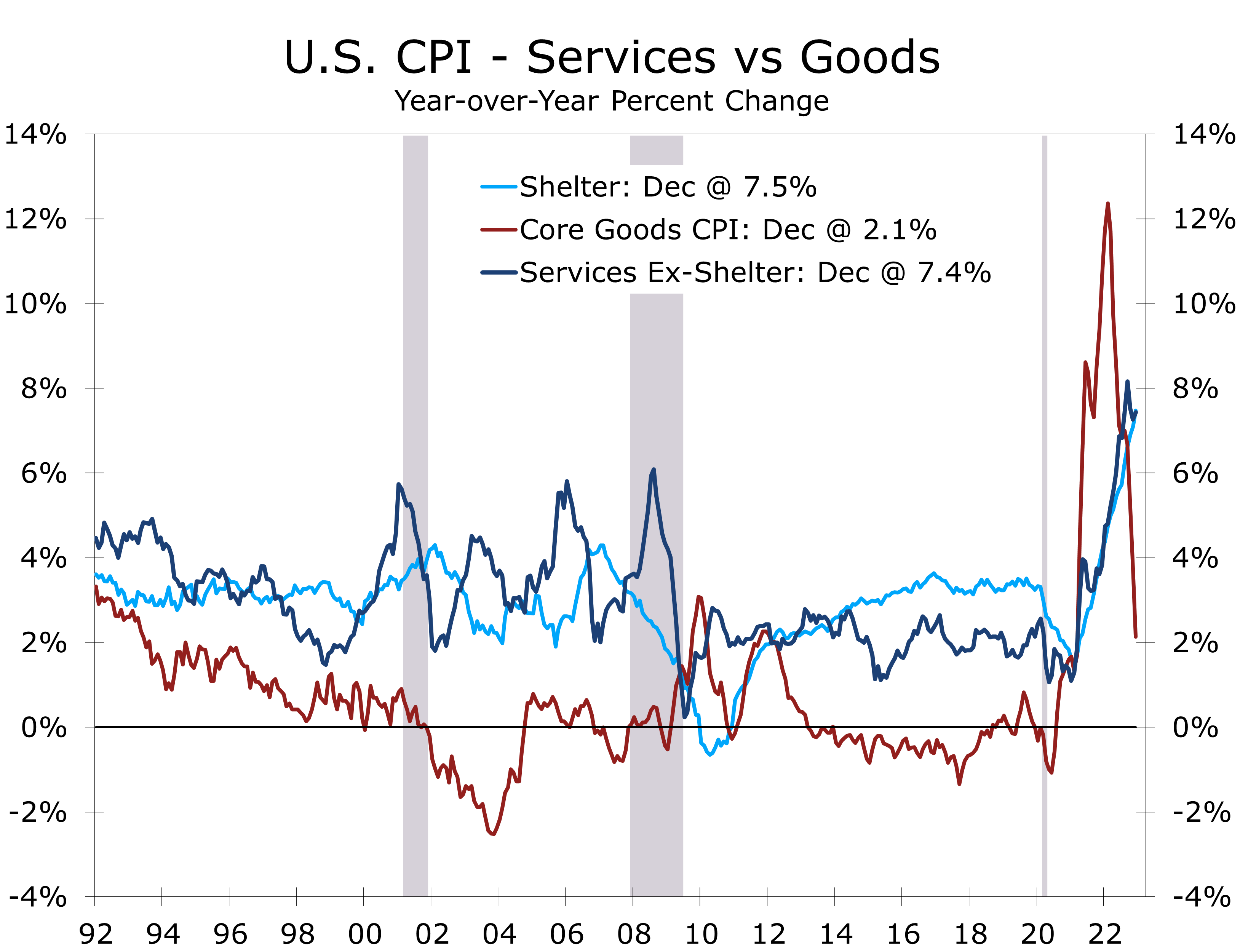

The Fed now sees the greatest risks to inflation coming from wages rising significantly faster than productivity growth due to the incredibly tight labor market. Chair Powell noted the disinflation process was now well underway, with consumers backing off goods purchases, which has helped ease supply shortages. Housing costs are also beginning to moderate. Powell described this as completing about half the job in bringing inflation back down. The key issue now is price pressures in more labor intensive parts of the service sector, with one of the key variables to watch being consumer prices for services, excluding shelter.

Powell’s tone in the press conference was considerably more balanced. While the inclusion of “ongoing increases” in the Fed’s statement remains consistent with the dot plot released in December, showing two more quarter point federal funds rate hikes, Powell did not put down the financial market’s notion the Fed only has one more rate hike. He reconciled the difference as to financial market participants perhaps being more optimistic about inflation coming down than members of the FOMC currently are.

Powell also appears to have shrugged off the recent easing in financial market conditions. Stock prices rose solidly in January, while bond yields declined. With consumer spending and industrial output declining, the Fed may now see an easing in financial conditions as something that would make a soft landing more likely. By contrast, Powell’s terse press speech at the Jackson Hole conference was widely seen as a warning to the financial markets to not get ahead of themselves and price in lower inflation and a Fed pivot. Today, the Fed is likely relieved mortgage rates have backed off their recent highs, which should help stem to slide in home sales and single-family home building.

The Fed now sees easing financial conditions as something that will help achieve a soft landing.

Powell mentioned the FOMC reviewed the latest Job Openings and Labor Turnover Survey (JOLTS) reported this morning. The data showed a surprising 572,000 increase in job openings in December. Most of these openings were in the leisure and hospitality sector, which includes hotels, restaurants, and entertainment venues – all of which have struggled to rehire staff following the pandemic. Job openings in the IT sector and manufacturing both declined in December.

While the Fed would like to raise rates a couple more times and bring the federal funds rate above 5%, the window for them to do so may not remain open that long. We doubt the Fed will continue to raise interest rates once nonfarm employment begins to decline, which we believe may occur before the May meeting.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.