Solid Jobs Data Boost Odds for A Soft Landing

- Employers added 223,000 jobs in December, which was close to market expectations.

- Job gains were broad based but continue to be led by industries still struggling to rehire workers lost during the pandemic, including many low-paying occupations in leisure and hospitality, health care, social assistance, and other services.

- Payroll gains for the prior two months were revised slightly lower. Employers added an average of 263,000 jobs per month in Q4 and added 4.5 million jobs in all of 2022, down from 6.7 million in 2021.

- Household employment posted an outsized 717,000-job gain in December, which helped lower the unemployment rate to 3.5%.

- Average hourly earnings rose a more modest 0.3% in December, which pulled the year-to-year gain down to 4.6% from a downwardly revised November level.

December’s employment data show job growth and wages moderating in a way that is more consistent with a soft landing. Nonfarm payrolls rose largely in line with expectations, with employers adding 223,000 jobs in November and gains for the prior two months revised lower by 28,000 jobs. December’s increase was close to the 263,000-jobs added on average for the past 3 months, particularly if you account for 36,000 workers on strike during the month.

Job gains continue to be broad based. The nonfarm diffusion index fell 2.2 points to a still healthy 60.7. Any reading above 50 means more industries added jobs during the month than reduced staff.

While a wide assortment of industries are adding jobs, the bulk of job gains continue to come from lower paying industries where payrolls fell the most during the lockdowns and struggled the most to rehire after the economy reopened. Leisure and hospitality added 67,000 jobs, accounting for just over 30% of December’s gain. Another 54,700 jobs were added in health care, and social services added 19,700 jobs.

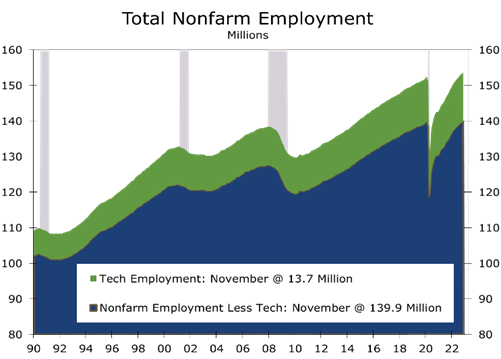

Given the growing number of tech layoffs, considerable attention is fixated on tech employment. While some analysts have emphasized the tech sector accounts for only a small share of nonfarm payrolls (8.9% based on the latest BLS data), the sector punches well above its weight. Tech employment, which we define as information services and professional and technical services, added 11,600 jobs in December.

Tech payrolls generally rose throughout the pandemic. The tech sector now employs 1,080,700 more workers than it did prior to the pandemic. Without the tech gains, nonfarm payrolls would have just surpassed their pre-pandemic highs this past month and would be a paltry 158,300 jobs above their prior peak.

Even amidst a surge in hiring at restaurants, bars, hotels, health care and other services this past year, the tech sector still accounted for an outsized share (13%) of overall job gains. The latest count of tech layoff announcements by Layoffs.fyi show intentions to cut at least 150,000 jobs, or about 10% of the jobs added in the tech sector since the start of the pandemic. Dismissing the rising tide of tech layoffs as merely a payback for over hiring during the pandemic seems overly simplistic.

The latest count of tech layoff announcements show intentions to cut at least 150,000 jobs

So far there has been little evidence tech layoffs are impacting the overall economy. This may be due to time lags between announcing and implementing layoffs. We may also find that job growth has been weaker than reported in subsequent revisions. This past month saw a flurry of reports highlighting what looks like a significant slowing in the Quarterly Census of Employment and Wages (QCEW) during the second quarter of 2022. The first quarter QCEW data, which were quite strong, are the basis for the annual employment revisions, which we will be released with the January employment report next month. BLS has already provided a preliminary estimate showing overall payrolls should be revised higher by 462,000 jobs and private payrolls revised higher 571,000 jobs.

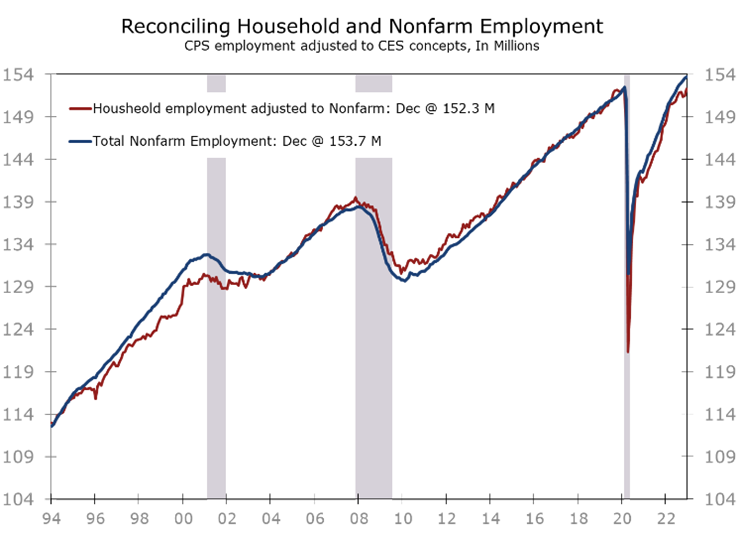

The Q2 2022 deceleration in QCEW employment growth will not figure into the revision process until February 2024. By then, we will have several more quarters of QCEW data. We suspect future QCEW reports will confirm that hiring has slowed significantly more than the current nonfarm employment data indicate. The household employment data might provide some guidance on what to expect.

Household employment, which comes for the Current Population Survey (CPS), is more volatile than the more widely followed nonfarm employment data, which comes from the Current Employer Statistics (CES) program. While December’s household employment data were indisputably strong, with the number of employed rising by 717,000 and the unemployment rate falling to 3.5%, the underlying details still show the labor market losing momentum.

The BLS reconciles the household series so that it can be compared to the nonfarm series. On this basis, December’s data were even stronger, with household employment rising by 826,000 in December. For the quarter, however, household employment adjusted to the nonfarm payroll standard was essentially unchanged. Moreover, a gap has opened since March of last year, with household employment rising by 1.8 million jobs, while nonfarm payrolls added 4.5 million jobs. The markedly slowed household employment growth since March might set the economy up for a surprisingly larger downward revision to employment in February 2024. We will not have to wait that long for clarification on this matter. The QCEW data is published quarterly and BLS will provide an early estimate of the 2024 revision in August.

Reconciling Household and Nonfarm Employment

There were several other positive aspects to December’s employment report. The unemployment rate fell to 3.5% in December, reaching its lowest level since December 1969. Both the labor force participation rate (62.3%) and employment-population ratio (60.1) rose by 0.1 point, and the employment-population ratio for prime working age persons rose 0.4 points to 80.1%, returning to the level it averaged during the middle of last year.

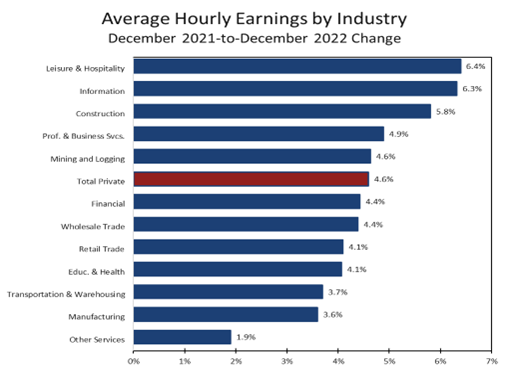

A great deal of attention was focused on the deceleration of average hourly earnings. Average hourly earnings rose just 0.3% in December and the prior month’s increase, which had initially been reported at 5.1%, was revised to 4.8%. The December data put the year-to-year gain at just 4.6%. While the deceleration in wages is welcome, we suspect much of the recent deceleration is due to changes in the composition of jobs being added. A disproportionate share of job gains the past two months have been in lower paying industries, primarily restaurants, bars and entertainment venues, and lower paying parts of health care and social services.

We suspect much of the recent deceleration in wage gains is due to a shift in the composition of job growth toward lower paying industries.

Wages are still rising the fastest in industries where demand for workers is the strongest. The leisure and hospitality sector added 67,000 jobs in December and added an average of 79,000 jobs a month in 2022. The industry added an average of 196,000 jobs in 2021. Despite the surge in hiring, leisure and hospitality payrolls remain 932,000 jobs below their February 2020 pre-pandemic level.

Restaurants, bars, and entertainment venues are still scrambling to find the workers they need. Wages have risen 6.4% over the past year to $20.64 an hour, which is the largest increase of any industry but also the lowest hourly wage. Average hourly earnings in the information sector, construction, professional and business services and mining and logging also saw wages rise faster than the 4.6% overall increase.

December’s solid employment data have increased the chances the Fed might be able to navigate a narrow road to a soft landing. The more cyclical parts of the economy – construction, manufacturing, and mining – added a combined 40,000 jobs in December. Employment in transportation and warehousing edged higher as well, although there was a 3,000 job loss in warehousing and a 4,400-job loss among couriers.

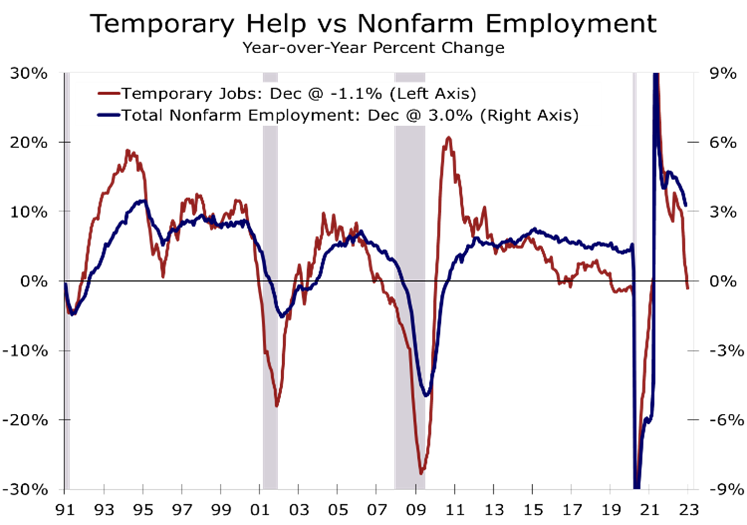

Aggregate hours worked in the factor sector fell 0.6%, suggesting industrial production in manufacturing likely declined in December. Employment at temporary staffing firms, which often leads nonfarm employment, fell by 35,000 jobs, marking its fifth consecutive drop. We still look for the Fed to raise the federal funds rate target by a half percentage point at the February 1 FOMC meeting.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.